A Utah Ridge Was His Favorite Spot as a Kid. Years Later, He Made It His Home.

An architect and his partner spent $3.9 million building a Z-shaped house just outside Salt Lake City By Laura Hine | Photography by Joshua Tug Ferguson for WSJ July 23, 2026 1:20 pm ET When he was a child, Steven Christensen would ride his bike on the dirt trails surrounding his family’s home in

Read More-

The 1,200-square-foot house has three decks and nautical details throughout KRISTIE WOLFE By Erika Mailman July 23, 2026 3:00 pm ET It has all the makings of a pirate’s hideaway: a ship-shaped house, a private island and a dock on an Idaho lake. The resemblance isn’t acciden

Read More Wall Street is selling more rental homes, as buying ban takes effect

Published Tue, Jul 21 20268:56 AM EDT Updated Wed, Jul 22 20268:57 AM EDT By: Diana Olick Property Play: Rental companies selling more property following new housing legislation A version of this article first appeared in the CNBC Property Play newsletter with Diana Olick. Property Play covers

Read MoreMortgage rates are rising again, but homebuyers are seeing some advantages

Published Wed, Jul 22 20267:00 AM EDT Updated Wed, Jul 22 20267:31 AM EDT By: Diana Olick A “Coming Soon” sign outside a home for sale in Hercules, California, US, on Wednesday, June 17, 2026. David Paul Morris | Bloomberg | Getty Images Mortgage rates continued their climb last week, but homebuye

Read MoreHome Price Growth Slowed Down. That May Be Changing.

After more than a year of headlines talking about how home prices are going to crash, the latest data shows that price growth may be starting to pick back up again. And depending on whether you’re buying or selling, that shift means something different for you.The Numbers May Be Starting To TurnFor

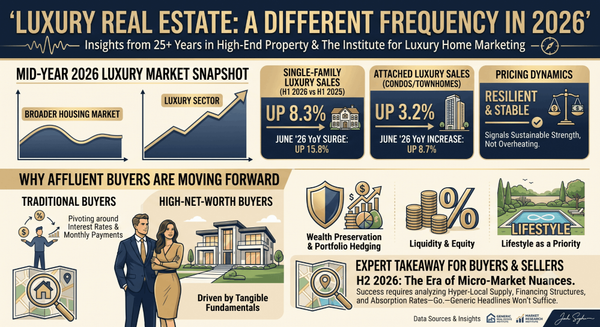

Read MoreThe Mid-Year 2026 Numbers at a Glance

In my 25+ years in high-end real estate, if there’s one lesson I’ve seen play out through every market cycle, it’s this: the luxury sector operates on a completely different frequency than the broader housing market. While many industry watchers predicted a cooling trend for 2026 due to persist

Read MoreSelling a Luxury House? Here’s Why Now Is a Good Time

If you own a luxury house, you're in a stronger spot than most sellers right now. While much of the market has cooled, the high-end tier hasn't. Sale prices and buyer demand are both up. So if you're considering selling, now could be a great time to make your move.Luxury Is Leading on PriceLet’s sta

Read MoreThe House That Started It All Could Kickstart What's Next

Remember how exciting it was to buy your first place? It felt like crossing a long-awaited finish line. It gave you a place to build your life. Maybe it’s where you lived when you got married. Or where you welcomed a child or a pet into the family.But that was just the beginning.For most people, you

Read MoreJUST SOLD: 7 Eagle Drive, Dartmouth, MA 02748

Experience the pinnacle of coastal sophistication in South Dartmouth’s most coveted gated enclave. This shingled contemporary masterpiece, custom-crafted by Fisher and Rocha and featured in Builder/Architect Boston magazine, rests on a private acre abutting the 3rd Fairway.A dramatic foyer leads

Read MorePriced Out? A Condo or Townhome Could Be Your Way In.

Today's home prices have a lot of buyers – especially first-time buyers – wondering if there’s even anything out there that’s in their budget. But owning a home may be more within reach than you think. Sometimes, it just means considering a different type of home.Condos and townhomes can be a great

Read MoreJUST SOLD: 125 Old Mendon Road , Cumberland, RI 02864

connected to town water and sewer. This thoughtfully improved residence offers modern systems, and resort-style outdoor living.Major upgrades include roof, heating and central A/C in 2024, upgraded electrical, newer hot water heater, and a new dehumidifier. Anderson windows, freshly painted interi

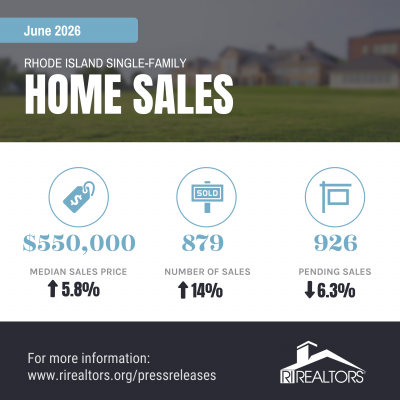

Read MoreRhode Island Real Estate Report: June 2026 Hits Record Highs

The summer housing market across the Ocean State is in full swing, and the June 2026 sales figures from the Rhode Island Association of REALTORS® show remarkable strength. Despite broader economic uncertainties and persistent interest rate headwinds, buyer demand in Rhode Island pushed single-fami

Read MoreMore Homes, Better Prices: A Buyer’s Summer

If you’ve thought about buying a home in the past few years, you may have run into two frustrations: asking prices that kept climbing and too few homes to choose from.In many places, both sticking points are letting up this summer, with lower asking prices and more homes for sale. Let’s look at the

Read More14 Years Running: Why Real Estate Is Still America’s Favorite Investment

Quick gut reaction. Which investment do Americans trust more than stocks, gold, savings accounts, and bonds? The answer hasn't changed in 14 years. It's real estate. And this year, that answer comes with even more conviction behind it. New data shows people aren't just saying homeownership is a smar

Read MoreThey Traded America for a Remote Archipelago. Now They’re Moving Back.

The couple is listing their Norwegian farmhouse after culture shock and logistical challenges prompted a return to Montana CHARLES POST By: Jessica Flint July 7, 2026 1:45 pm ET An American couple who spent more than six years and tens of thousands of dollars living out an Arctic real-estate fanta

Read MoreGen Z and Millennial Collectors Turn Vintage IKEA Into Investment Pieces

The Enetri, a 1980s linear bookshelf from IKEA, in Alex Greene’s apartment. The piece is also called the Guide. Once-cheap furniture now fetches thousands of dollars on the resale market By Leonora Epstein | Photographs by Evan Angelastro for WSJ July 8, 2026 12:05 pm ET In 1971, the affordable Swed

Read MoreFar more real estate agents now report seeing a balanced market, CNBC Housing Market Survey finds

Published Tue, Jul 7 20267:00 AM EDT Updated Tue, Jul 7 202612:03 PM EDT By: Diana Olick A version of this article appeared in the CNBC Property Play newsletter with Diana Olick. Property Play covers new and evolving opportunities for the real estate investor, from individuals to venture capital

Read MoreNew housing law targets affordability — what it means for homebuyers and sellers

Published Sat, Jul 11 20269:30 AM EDTUpdated Sat, Jul 11 20269:41 AM EDT By: Sarah Agostino & Mike Winters How the new housing law plans to fix the housing crisis Bipartisan legislation intended to increase the U.S. housing supply and improve affordability is now law — but experts say homebu

Read MoreThink Nobody's Buying Homes Right Now? Think Again.

If you've been thinking about selling, you've probably seen plenty of headlines suggesting buyers have just about disappeared. But there's a big difference between a slow market and a stalled one.Yes, mortgage rates are still higher than most people would like. Homes aren’t selling as fast as they w

Read MoreThe “Take It or Leave It” Attitude Is Fading from the Market – What That Means for You

Negotiations are back. More buyers are asking for better deals, and more sellers are giving them. Builders are throwing in extras, too. That’s why whether you’re buying or selling today, there are two terms you’ll hear a lot: concession and incentive.A concession is something a seller agrees to duri

Read More

Categories

Recent Posts